Table of Contents

M&A deals are often treated as markers of growth in logistics. But the wave of consolidation at the top of the UK 3PL sector tells a more complicated story when set against rising insolvency rates among smaller transport operators.

The UK logistics and third-party logistics (3PL) sector is being reshaped from both ends. At the top, a string of high-profile mergers and acquisitions is concentrating market share among fewer, larger players. GXO's purchase of Wincanton, CMA CGM's acquisition of Bollore Logistics, the DHL eCommerce UK and Evri merger and InPost's takeover of Yodel have all redrawn the competitive map. At the bottom, smaller hauliers and transport companies are folding at rates well above pre-pandemic norms.

This article looks at what's driving both trends and where platforms like FLOX fit in.

Opportunities: Streamlining Efficiency, Expanding Reach

Mergers and acquisitions can improve operational efficiency through resource consolidation and the elimination of redundancies. GXO's acquisition of Wincanton is a good example. The UK Competition and Markets Authority (CMA) cleared the deal subject to the divestment of a small number of Wincanton grocery contracts. GXO expects full annual net run-rate cost synergies of GBP 45 million (pre-tax) by the third year of integration. That's a concrete number behind the standard "efficiency gains" claim.

The deal strengthens GXO's service offering by adding Wincanton's deep UK network, particularly in sectors like defence and aerospace where Wincanton held established contracts. Post-acquisition, GXO's share of the UK contract logistics market increased by roughly 5%.

These mergers also expand service portfolios and open new geographies. CMA CGM completed its EUR 4.85 billion acquisition of Bollore Logistics and folded it into CEVA Logistics, creating the world's fifth-largest logistics operator. That deal boosted CMA CGM's capabilities across Africa and Asia-Pacific, markets where demand for freight forwarding and contract logistics is growing fast.

The DHL eCommerce UK and Evri merger, completed in October, created one of the UK's largest parcel operations. The combined business handles more than one billion parcels and a further one billion business letters per year, with a fleet of 8,000 vehicles and over 30,000 couriers. For shippers, this kind of scale means broader delivery coverage and more competitive pricing.

“The big acquisitions get the headlines, but the real test is what happens 18 months later when two sets of systems, cultures and customer expectations need to work as one. That integration gap is where shippers feel the pain - and where multi-party platforms add the most value.”

Michael Ostroumov, Co-founder, FLOX

Challenges: Navigating Integration and Maintaining Service

Consolidation raises legitimate concerns about reduced competition. Fewer large players can mean higher prices and less choice for shippers, particularly in segments where one operator dominates.

The integration process itself carries risk. Merging two logistics operations means aligning warehouse management systems, transport management platforms, customer contracts and staff structures. During this transition, service disruptions are common. The CMA imposed conditions on both the GXO-Wincanton and DHL-Evri deals specifically to protect competition in affected market segments.

Post-acquisition of Wincanton, GXO's share of the UK logistics market grew by 5%, concentrating market power further. For customers tied to long-term contracts, the practical question is whether the acquiring company will maintain the same service levels, pricing structures and account management relationships that the acquired business offered.

The parcel sector faces a similar dynamic. Evri's absorption of DHL eCommerce UK brings operational scale but also complexity. DHL eCommerce UK will be rebranded as Evri Premium, operating as a separate network for time-sensitive and high-value deliveries. Whether that two-tier structure delivers a better experience for retailers remains to be seen.

Challenges Leading to Insolvencies Among Smaller Transport Companies

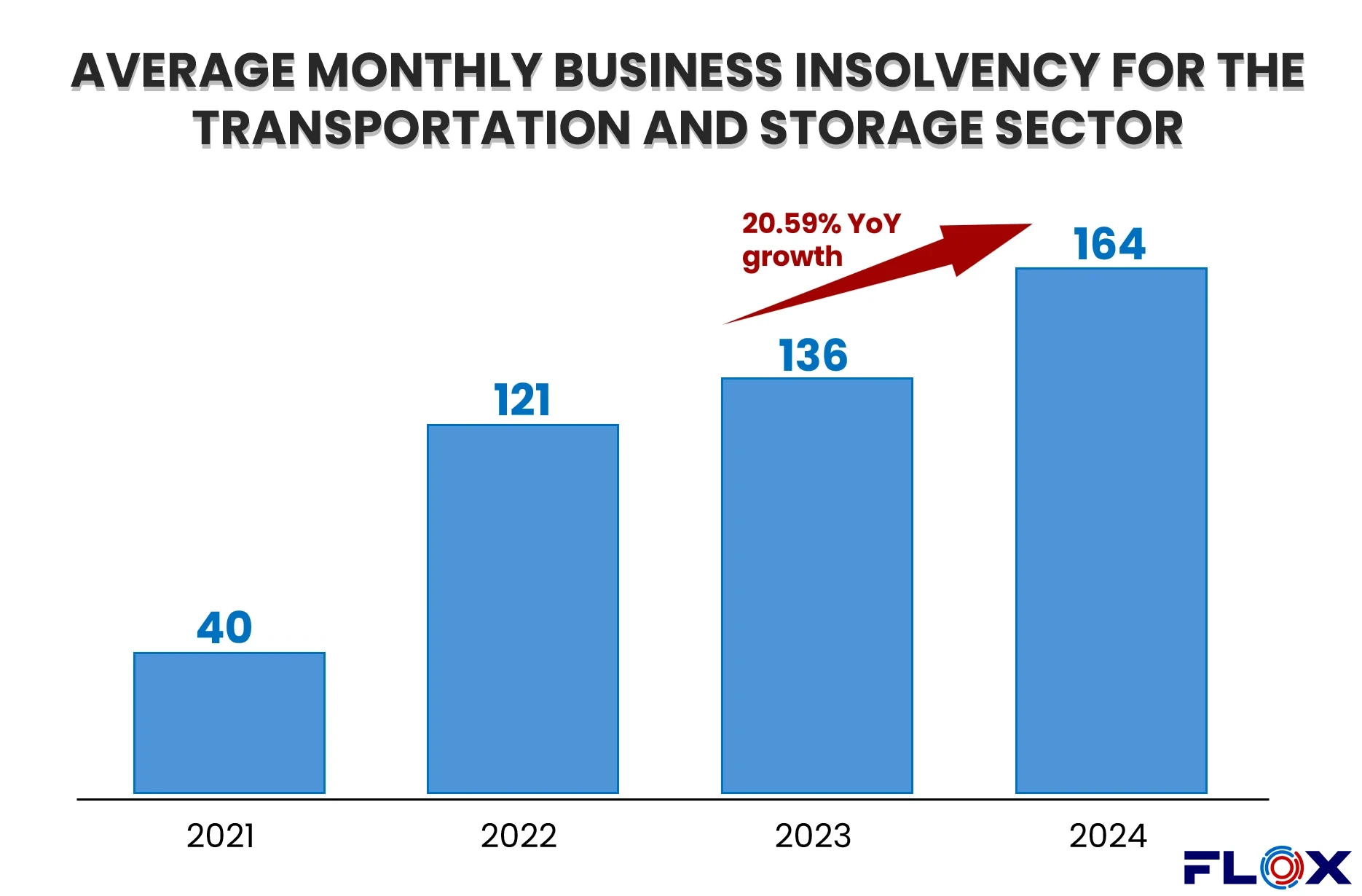

The other end of the market is under severe pressure. Smaller transport companies are facing insolvency rates that remain well above historical averages. UK road haulage insolvencies rose from 1,068 across the five-year period to 2020 to 2,051 across the following five years. The peak hit 503 insolvencies in a single year before dropping to around 400, but that figure is still double the pre-pandemic baseline.

Several factors are compounding:

- Rising operational costs: Fuel accounts for up to 30% of operating costs for haulage companies, according to the Road Haulage Association. The RHA also reports that the average profit margin across the haulage sector sits at roughly 2%. The cost of running an HGV fleet has increased by around 10% year-on-year. For smaller operators with thin reserves, that arithmetic is brutal.

- Regulatory pressures: Compliance with environmental regulations and safety standards requires investment in newer, greener fleets. Transport for London introduced new safety standards for vehicles over 12 tonnes with less than a year's notice. Operators running vehicles with life cycles of seven or more years face expensive upgrades they may not be able to afford.

- Competitive pressure: Larger 3PLs can offer more competitive rates through economies of scale, squeezing smaller operators out of contracts they previously held.

- Cash reserve crisis: ONS data shows that 36.8% of transport and storage companies have no cash reserves at all. A further 12.4% report less than one month of available financial resources. The number of transport and storage businesses fell 9.1%, with freight transport by road down 15.5%.

Maddi Solloway-Price

Head of Road Freight at Logistics UK

Chain Reaction Podcasts

The Human Cost of Road Freight

Behind every delivery is a driver working long hours with limited recognition. Maddi challenges an industry obsessed with automation to remember the people keeping freight moving.

For SME logistics operators, M&A presents a strategic choice with no easy answer. Aligning with a larger entity or consolidating with peers can offer access to broader networks, better technology and more capital. But the trade-offs are real: loss of control, dilution of company culture and the challenge of integrating into complex enterprise systems. Any M&A decision needs to align with long-term strategic goals, not just short-term financial pressure.

The M&A Wave Beyond the Mega-Deals

The headline transactions - GXO-Wincanton, CMA CGM-Bollore, DHL-Evri - represent one tier of consolidation. But mid-market M&A activity is also accelerating across UK logistics.

InPost's acquisition of a 95.5% stake in Yodel made the Polish parcel-locker operator the third-largest independent e-commerce logistics provider in the UK, with an estimated 8% share of the parcel market. CMA CGM is also acquiring Freightliner UK Intermodal Logistics, expanding its rail freight presence and supporting a shift towards lower-carbon transport modes.

The pattern is clear: international logistics groups are buying their way into UK market share. For domestic operators who aren't acquisition targets, the competitive pressure is intensifying. And for shippers, the question is whether fewer, larger providers will deliver better service or just more concentrated pricing power.

FLOX: Supporting Both Ends of the Logistics M&A Market

These industry shifts create a clear role for multi-party logistics platforms. FLOX connects shippers with warehouse providers, 3PLs and hauliers across the UK and Europe, operating as a virtual 4PL that combines discovery, execution, visibility and financial control in a single platform.

For larger 3PLs navigating post-merger integration, FLOX offers a way to optimise expanded networks. During the transition period when systems are being merged and capacity is being rebalanced, efficient matching of demand with available capacity helps prevent the service disruptions that typically follow acquisitions.

For smaller transport companies facing the pressures described above, FLOX provides access to a broader pool of potential customers without the overhead of building those commercial relationships from scratch. Better load factors and more efficient fleet utilisation directly improve margins, which for operators running at 2% profitability can make the difference between survival and insolvency.

The platform's multi-party approach matters here. Rather than forcing operators into a single carrier's ecosystem, FLOX enables collaboration across a network of providers. That's a different model from the consolidation happening through M&A. It gives shippers optionality that a market dominated by a handful of mega-operators can't always provide.

Explore storage and fulfilment solutions that give your business flexibility and the support it needs to grow.

Building Resilience in UK Logistics

The UK's logistics and 3PL sector is being pulled in two directions. Consolidation through mergers and acquisitions in UK logistics is concentrating market power among fewer operators. Insolvency rates among smaller hauliers, while off their peak, remain at levels that point to structural problems in the economics of road freight.

Both trends create risks for shippers. Over-reliance on a single consolidated provider brings concentration risk. And the disappearance of smaller operators reduces the flexibility and local coverage that many supply chains depend on.

Platforms like FLOX sit between these two forces, connecting shippers with 3PLs and logistics providers of all sizes and helping both sides of the market operate more efficiently. In a sector where the biggest players are getting bigger and the smallest are under existential pressure, that connecting layer is becoming harder to do without.

Subscribe to our newsletter.

Stay up to date with practical insights and useful logistics content

FAQs

UK logistics M&A is being driven by international operators seeking scale and market access. Major deals include GXO's acquisition of Wincanton, CMA CGM's purchase of Bollore Logistics and the DHL eCommerce UK-Evri merger. Buyers are looking for consolidated networks, cost synergies and stronger positions in contract logistics and parcel delivery. The trend reflects a broader shift towards fewer, larger providers competing for market share across freight forwarding, warehousing and last-mile delivery.